What Does the Federal Reserve's Decision to Keep Rates Steady Mean for Your Money?

The Federal Reserve (the Fed) plays a big role in the economy by setting interest rates. In 2022, it raised rates to fight rising prices. Last year, it cut rates as price increases slowed down. Now in 2025, the Fed is keeping rates steady even though there are worries about trade tariffs, how consumers feel, and whether the economy might slow down. Let's look at why the Fed is taking this approach and what it means for your long-term savings.

The Fed has two main jobs: keeping unemployment low and prices stable. While the economy grew by 2.5% in 2024, it's expected to grow more slowly at 1.7% in 2025. Despite this slower growth forecast, the Fed is taking a careful approach and hasn't changed its plans for interest rates.

One big concern is that new trade tariffs might make some goods more expensive. However, the Fed sees this as different from the broader inflation that affects prices across the whole economy. For example, in 2018, washing machine prices went up because of tariffs but then leveled off.

The Fed is also looking at positive signs in the economy. There are plenty of jobs available, wages are going up, and people are still shopping, even though consumer confidence is low.

The Fed still plans to lower rates twice in 2025

Looking ahead, both the Fed and financial markets expect two or three rate cuts in 2025. However, these predictions can change quickly - at the start of 2024, markets expected seven to eight cuts, but only three happened.

The Fed has also decided to slow down its program of selling bonds, which is another way to support the economy. For long-term investors, it's more important to focus on the general direction of rates rather than any single Fed decision.

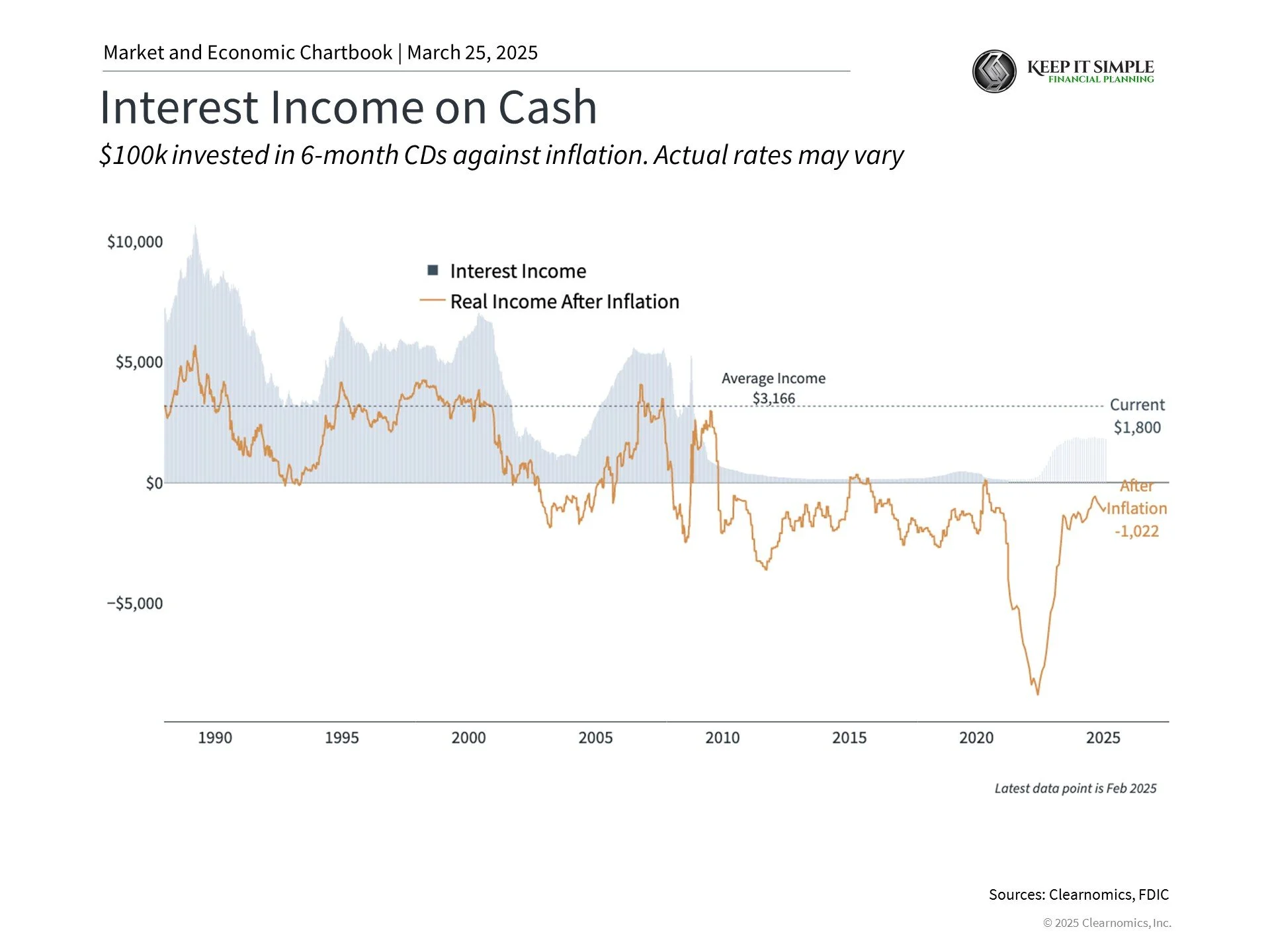

Keeping too much money in cash can hurt your long-term savings

When markets are uncertain, keeping money in cash might feel safe. But this strategy can actually work against you. Markets often recover when people least expect it, and missing out on these recoveries can harm your long-term financial goals.

Even though cash accounts are paying higher interest rates now, the real value of your money can still shrink because of inflation. While some savings accounts offer better rates, cash alone isn't enough to help your money grow over time.

The bottom line? The Fed is taking a balanced approach despite current worries about the economy. As a long-term investor, you should try to do the same. History shows that staying invested, rather than reacting to short-term news, is the best way to reach your financial goals.